Sunday Read: Would the Welsh Regions Make More Money in England?

An attempt to use data to answer this complicated question

There has been a lot of push from the Welsh rugby press lately for the Anglo-Welsh league, particularly by Steff Thomas of Wales Online who has written multiple articles on the topic.

The recent discourse has been centred around the financial viability of such a competition. The argument is that the Welsh Regions would make more money playing against English sides than they would staying in the URC.

In this article we will attempt to put some numbers to this discussion and attempt to understand what impact a switch of leagues may have on the Welsh Region’s finances by examining the current split of the respective TV deals, considering matchday income and forecasting future possible revenues based upon recent performance.

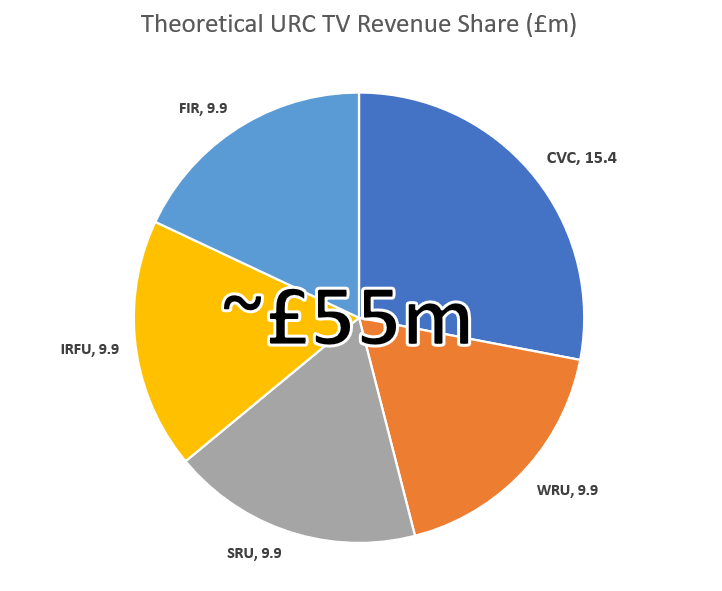

URC TV Revenue

It is very difficult to say how much the Welsh teams earn via the URC. The WRU are joint shareholders of the league along with the other member unions and CVC apart from South Africa who only become stakeholders next year. CVC own a 28% stake in the league and the unions own equitable shares of the rest.

The URC TV deal, according to the Financial Times, is worth £55m per season. Dividing this up as per the arrangement described above would suggest each Welsh Region is getting around £2.5m per season. There is also the payment South Africa are currently making to the league for the right to play in it, which stops next year. The value of this amount is not publicly know, but it is thought to be several million per season.

However, Wales Online claim that the regions are currently receiving less than £2m per season for playing in the league. It has been claimed in the past that all of the revenue from the URC is passed to the regions, so it is unclear where this discrepancy originates from.

For the sake of this article, we will make the assumption that the Welsh Regions are getting just under £2m per season, as Wales Online suggest.

How the Welsh Could Join the Premiership

The English clubs receive commercial revenue from Premiership Rugby through their P-shares. If the Welsh were to join the Premiership, one of 2 things would have to happen:

Premiership Rugby is disbanded and a new company is set up with the Welsh as equal partners, P shares would then be redistributed from scratch

The Welsh would have to buy into Premiership rugby

The more likely of those two is the latter. Most franchise leagues around the world have a buy-in cost, from Formula 1 to the MLS. As stated above, the South African franchises are still paying to play in the URC.

The cost of this buy in would be at PRL’s discretion. It would likely be several million pounds paid over multiple seasons. During this time, the regions would not be eligible to receive any commercial revenue from Premiership Rugby, nor would they have any say on the league’s governance.

The Welsh could buy some of CVC’s share off them, but this is unlikely given all of the dealings between the two so far have been the WRU selling to CVC. CVC would also look to sell their shares at a profit, with their initial stake being bought in 2018 for £230m (£8.5m per 1%).

Based on the the price CVC paid for their percentage of the Premiership, the estimated total cost of an equitable share in the league would be £177.5m. This is unlikely to be the the exact fee due a) inflation, b) the reduce commercial value of the league since CVC’s buy in and c) any mitigation offered to the Welsh regions due to the forecast increase revenue generated by having them in the league.

It is highly unlikely that the regions themselves would be able to afford whatever price the buy-in would be without securing additional outside investment several times greater than what they already have.

The bill could instead be paid by the WRU on behalf of the regions. The union does not have the cash reserves to fund this up front. It made a loss of £14m in the 2023 financial year and reported cash reserves of £44.2m at the end of the same period. It would therefore have to borrow the money and pay it back over several decades. The WRU currently owes existing creditors around £150m.

The other possibility would be a merger between the Premiership and the URC orchestrated by common stakeholder CVC. This would render most of the above points irrelevant, but speculating on potential details of such an arrangement is beyond the scope of this article. We will continue under the assumption the Welsh are leaving the URC and the two leagues will continue on separately.

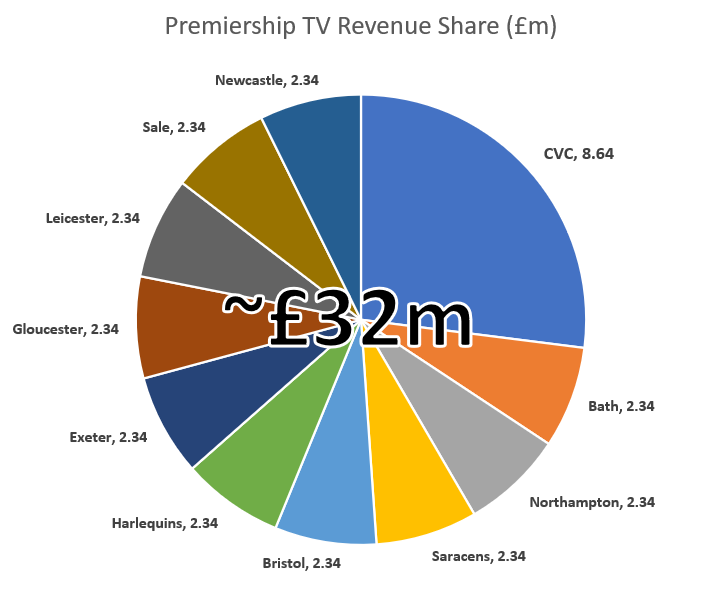

Premiership Rugby TV Revenue

The English Premiership has just signed a new TV rights deal with TNT sports which the Telegraph report is worth around £32m per season. Again, CVC own a portion of the league, this time 27%. The rest goes to Premiership Rugby Limited which is made up of the participating clubs. This puts the share of TV revenue to each of the 10 Premiership clubs at just over £2.3m.

It is clear that if 4 more teams were to be added to the league that the TV income would be heavily diluted unless the TV revenue were to expand accordingly. But how much would it need to expand by?

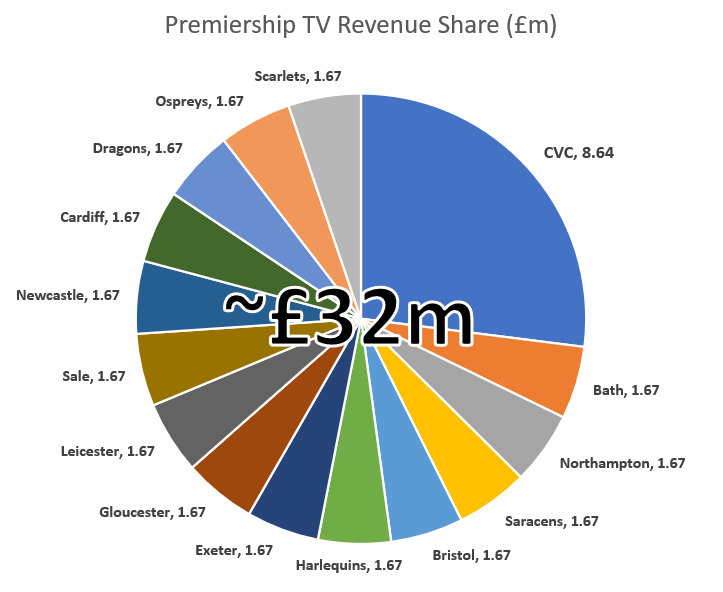

The Impact to the Premiership of Adding the Welsh

Assuming, though, that the 4 regions do manage to buy into the P-shares currently held by the Premiership clubs. If the TV revenue were to stay the same, the share of the money would look like this:

Clearly, this is a worse position than what is currently had in the URC and would be unacceptable to the Premiership teams as it represents a reduction of income of nearly 30%. However, it is reasonable to assume that the introduction of the Welsh teams would cause the value of the TV right to increase.

In order for the per-team-split to be maintained at the current level, the per season rights deal would have to climb to around £45m per season, a £13m (41%) increase on the current deal and a record level for the Premiership.

So, is this level of increase likely? There are a number of things to take into account when answering this question, including:

The increase of number of games from 93 to 187 (assuming a Top14 style double round robin format with quarter finals, semi finals and grand final)

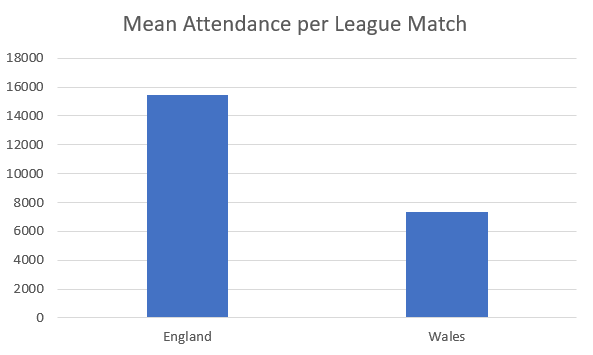

The potential market in Wales being just 6% of what it is in England (based on population size)

The fact Welsh Rugby matches must, by law, be shown in Welsh language which would most likely take the form of a free-to-air contract with S4C

The fact the elite rugby attendances for league matches in Wales were just 19% of what they were in England last season

There is little to no competition for TV rights in the UK, with even some England international matches going without a mainstream broadcaster

Based upon the data that is currently available, it appears unlikely that the addition of the Welsh regions to the English Premiership would, in the short term at least, generate the necessary uplift in TV revenue to offset the dilution caused by adding 4 teams as equal partners.

Matchday Revenue

Knowing the matchday income per customer (attending fan) for each club in England and Wales is close to impossible and would be a closely guarded secret for most. We know that matchday income is less than TV revenue income, with even the French Top14 seeing TV income from LNR averaging around 30% higher in value than matchday income. Looking outside of rugby, the ‘Welcome to Wrexham’ documentary suggested that an average of around 4,000 fans per game over a 44 game season resulted in a £2m increase in takings. This works out to around £10-12 per fan per game. The average price of a season ticket for the regions starts at around £210.

As we do not know the values of the matchday incomes of regions, for this article then we shall refer to the value simply as ‘x’. Assuming a double round robin format, each team would play an extra 4 home games per season. If we also assume that the attendance for those games would be in line with current attendances, the matchday income would rise by 44%. A significant amount.

Many argue that the Welsh regions would see an even greater increase as playing against the English sides would result in bigger crowds. Last season, Cardiff’s Champions Cup home games against Bath and Harlequins drew crowds of 12,000. By contrast, Osprey’s R16 game against Sale drew just 4,400. This is less than Dragons drew for their league match against Zebre (All data taken from URC official app). Cardiff’s own game against Sale last season drew around 7,000 which is similar to what they drew for their game against the Stormers in the URC this season.

Assuming a best case scenario where each Welsh region drew 12,000 per game - with the exception of the Dragons whose Rodney Parade venue has a capacity of just 8,700 - and that the Ospreys cancel their move to St. Helens where the capacity is not expected to exceed 8,000, the total attendance for region matches per season would grow to just over 581,000. This is a 121% increase. Therefore, the matchday income would be more than doubled.

Additional Context

The above analysis makes a number of key assumptions. In some cases, these assumptions are at a high risk of changing. These risks are as follows:

The TV commercial revenue of the English Premiership has been shrinking with the current TV deal with TNT being the at lowest value it has been since BT sport took the rights in 2013. The deal is has also reduced in length with each renewal, affecting the long term stability. The new deal is reported to be worth £1m per season per club less than the previous one

The number of English Premiership teams has reduced in recent years from 13 to 10. There have been rumours of financial instability at at least 3 more clubs. It is therefore possible the number of teams could reduce further. It has also been rumoured one Welsh team could go, although this currently looks unlikely.

It has been assumed that the Welsh regions would not be relegated from the Premiership once added to it. The League has been ringfenced in recent years but there is currently a push in England to reintroduce it. The English Championship currently has no broadcast deal whatsoever.

A double round robin format might be undesirable due to it’s length (the French Top14 ran from August to June) and the need for bigger squads to cope with the number of games. The alternatives would be URC or Super Rugby style pool systems or an MLR style conference system based on geography.

The WRU currently has a contract with the URC until 2028. If it were to leave this contract early, there may be additional charges payable to the URC.

The URC is currently experiencing growth, with each season so far exceeding the viewership and attendance of the season before. It is therefore likely that the TV revenue for the URC will increase moving forward.

It is also worth noting that the clubs currently in the English Premiership are all operating at a loss, with some losing as much as £5m in their latest accounts, more than twice as much as any Welsh Region. Premiership Rugby itself saw it’s equity shrink from £41m to just £5m from 2022 to 2023 while it ended the 2022/23 season with losses of £22m.

Additionally, leaving the URC could see the regions lose their place in the EPCR competitions. The WRU is not a stakeholder in EPCR, earning their place in the competitions solely through the URC. They could be invited back into the Challenge Cup as per Black Lion and Cheetahs currently, but they might not be eligible for the Champions Cup no matter what their league position was. This was the case for the Cheetahs and the Southern Kings in the Pro14 era. As with the URC, the South African franchises are currently paying millions of pounds per season to play in the EPCR competitions.

Travel Savings

The big saving to the Welsh of not playing in the URC would be the travel costs. The current format of the URC means that 12/18 games each region plays are in Wales, with all regions being within a 60 mile radius on the M4.

The saving from a travel point of view (excluding play-offs) would come from:

1 return flight to South Africa

1 domestic flight within South Africa

1 flight to Italy

I flight to Scotland

2 flights to Ireland

Associated hotel bookings for duration of stays

The number of games that the regions play outside Wales would increase from 6 to 10, but the assumption is that they would drive to all of these games. The possible exception to this would be the game against Newcastle Falcons, a flight to which would effectively be equitable to a flight to Scotland. The sum of the savings would likely be around £1m per region.

Findings

The analysis in this article is based around several assumptions and we have addressed the risks associated with them. It has been shown that if the Welsh regions were to move to the English Premiership they would save money on travel expenses.

A best case scenario would see close to a doubling in matchday revenue for the regions, but there is a considerable amount of data available to suggest this best case scenario is unlikely. However, the assumed increased number of home games alone would lead to significant increase of matchday revenue.

There would be three costs associated with the move itself, specifically:

The purchase of P-Shares to earn commercial revenue from the league

The necessity of a larger squad to fulfil a longer fixture list

Any early exit fee for the URC contract

These costs would likely be several million pounds per season over a number of seasons, akin to the deal the South African’s have currently, during which the regions may be ineligible to receive commercial revenue from PRL.

The TV revenue for the league would have to increase significantly from its current level to offset the increase in number of teams. Whilst an increase is almost certain, an increase to the required level is unlikely due to 2 factors:

The small size of the market in Wales

The lack of competition/demand for rugby TV rights in the UK

It is likely that the Welsh regions would be ineligible for a share of the TV revenue for a number of seasons as per the South African deal in the URC.

There are also 3 potential financial risks associated with leaving the URC.

Relegation to the Championship which does not currently have a TV broadcast deal

Exclusion from European competition preventing the Welsh teams potentially competing in the Champions Cup or necessitating the buy-back-in to the EPCR

Missing out on any increased revenues the URC are able to generate based on the year on year growth the competition has seen so far

It is highly unlikely that the Welsh would be granted immediate power to change the rules in England to prevent these things from happening.

Conclusion

Should the TV rights value remain relatively similar to what it is now, it is possible that the increased matchday revenue combined with the reduced travel costs could see the Welsh regions be slightly financially healthier playing in England.

However, there is a high chance these gains would be offset or even superseded by the cost to buy into the league, the exclusion from commercial revenue until the buy in is complete and the damage of possible relegation to the Championship and exclusion from Europe.

Even when they became equitable partners in the league, it is still likely the regions would continue to operate at a loss, as are all of the clubs currently playing in the English Premiership.

From an English point of view, it is a simple business case decision: Would the increase matchday revenue and increase in TV rights value offset the dilution in commercial revenue due to the increase number of teams without damaging the integrity of the product?

Thanks for reading! Help us spread the word of our YouTube channel, aiming for 2k subs!